How the financial world models "value"

The building blocks of a robust player evaluation process can be found in corporate finance.

I would hope at this point you are convinced of the need for a GM to align and cascade his overall objective down to every layer of his organization and measure all important decisions based on their impact to the team’s goal difference in the seasons to come. Hopefully, you also found it persuasive that critical insights should be generated by club experts and then denominated in this same unit of goal difference so as to easily transfer them into the decision making process without much loss in utility. But, setting up this framework within the soccer operations department of a club is no easy task. Distilling the most complex of all footballing personnel decisions down to a single “go/no-go” decision based on a single metric is difficult, especially given the mysteries of soccer, the dynamic and fluid structure of the game, the uncertainties that abound and the nature of the data that is recorded for each match. But, because these exact challenges face the business and financial communities every day, and because these communities prefer to make money, they haven’t just shrugged their shoulders and given up. They’ve instead built a theoretical and practical framework for dealing with these difficulties, and our sporting director can learn from such a framework.

In this post, I’ll try my best to summarize the key concepts you’ll find in any good Corporate Finance textbooks and in practice about “how to value something.” Then in the articles to follow, we will map them over to the player recruitment work stream within a soccer operations department. As you’re reading through this post, please take at face value the concepts as they might operate in the financial world, but if you can, hold in your periphery the issues facing a sporting director as he works to build a squad to meet his club’s needs.

The Model

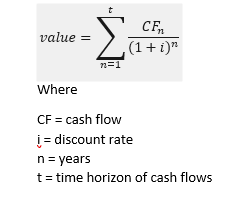

The corner stone of corporate finance is the discounted cash flow approach to value. Stated simply, as a general rule the value of a thing is the sum of all the estimated incremental cash flows it will generate in the future, “discounted” back via some math to a present value. The math uses a “discount rate” to take into account the risk and the timing of each cash flow and the opportunity cost associated with the investment and in doing so “holds the price of the investment responsible” for such risks/costs. For a given stream of expected cash flows, the higher the risk, the lower the price. If I knew Greek and how to do fancy academic stuff, an example of the value of an investment that yields one payment each year over a number of years might be expressed like this:

At its core, the way this works is that you an investor have some cash on hand and you want to invest it for some reason. The investment you’re looking at has an expected stream of cash flows associated with it in the future and because the future is uncertain, the investment opportunity has a certain risk attached to those cash flows (these cash inflows may not occur or they may occur in amounts that differ from your estimate to your benefit or to your detriment). Because you have innumerable options to invest in, there is an opportunity cost associated with you investing in one investment instead of a different one. This opportunity cost is captured via the “discount rate” used to discount the estimated future cash flows back through time to the current moment (the moment where you have to pony up the cash for the investment via a price, where you pay for the value). The discount rate is normally expressed as an annual percentage yield (e.g. 8%), and can also be referred to as the “required rate of return” because it is essentially the annual rate of return that a similarly risky investment opportunity out there is offering over a similar time horizon. Riskier cash flows are generally “discounted” at higher rates, which is intuitive because in an uncertain world, you an investor when faced with two different investment alternatives, each with the same expected value and timing of future cash flows would choose the less risky one, and you would only pay a discounted price for the riskier one if the other was also available. The riskier investment because its price is now discounted is able to meet the “rate of return” you require of it (i.e. it has been discounted using the required rate of return). Here’s a picture of Brad Pitt to cleanse.

Net Present Value

Even if this basic framework is somewhat abstract, one of the benefits is that once you re-arrange the equation, it boils down the value model into a really basic decision point. If you take the equation above (some stream of cash flows discounted at an appropriate rate) and then add a fixed cost that you have to pay to acquire said cash flows as an initial negative cash flow into the model (i.e. you subtract the cost of the investment), you get what is known commonly as the equation for “Net Present Value.”

And the beauty of the theory behind “Net Present Value” is that at a conceptual level, investing in something with a positive “NPV” (i.e. you pay less than the present value of its expected future cash flows) immediately increases your wealth (even before the cash flows arrive or don’t, since they’ve already been discounted back through time), while choosing to invest in something with a negative present value (you overpay) immediately decreases your wealth dollar for dollar.

As you can see, while there are a ton of assumptions that go into the equation, namely the uncertainty of estimated future cash flows and the judgment that goes into determining the required rate of return, the output of the model is a perfectly digestible “go” or “no-go” decision. So long as you have the money to invest, theoretically any investment with an NPV greater than or equal to zero is a “go” and any investment with an NPV less than zero is a “no-go.” With the theory in place, the joy/suffering of the financial/business world could in part be reduced to the search for these positive NPV opportunities, whether an individual actor follows this exact template or use a short-hand, or neither.

In practice, the financial world at times devolves from the practice of estimating value and calculating prices in this manner to some ugly derivative of it, speculating instead on future changes in prices* driven by the psychology of others (Keynes). But the underlying theory of value is still present, and besides this is a feature that we do not need to map over analogically to the football problem of estimating player performance, so for now, we can rather discreetly look the other way.

*(do read Zach Carter’s The Price of Peace on John Maynard Keynes if you have not)

Capital Budgeting: Which Projects to Undertake

The same process we walked through above can be mapped from a single investor choosing between various investment opportunities to a business that is evaluating various internal projects, all of which require varying levels of upfront investment (initial negative cash flows) and all of which can be said to generate streams of incremental expected cash flows which vary in their amount and timing. A crucial difference is that while an investor must weigh the available investment opportunities and the risks and rewards attached to each, a business isn’t an investor but it has investors — investors which require a certain rate of return back from the business, given the overall risks associated with the cash flows they expect the business to generate for them. And the business also has creditors — creditors who expect the company to pay certain cash flows to them as legally bound in their related debt agreements. So, when a business is choosing between available projects to undertake, it estimates the future cash flows associated with the project as described above, but the “required rate of return” that it uses to discount the cash flows is what is known as the “weighted average cost of capital” which is essentially the weighted average of the required rates of return its investors (return on equity) and its creditors (return on debt) are “demanding” of the business as a whole. Nathan Tankus wrote just this week in his Notes on the Crises about how practically, this comes in the form of a “hurdle rate” that is set by the CFO that perhaps rarely changes for a company. Anyhow, any project that generates cash flows exceeding the returns required by its investors and creditors on the whole (or that exceeds the related hurdle rate, set directionally by these things) is a “go” so long as the business has access to enough capital to make the required upfront investments. This process of evaluating various available investment projects and allocating available capital between positive net present value projects and rejecting negative net present value projects is known as “capital budgeting” and it is critical to the value of a business. The reason for this is, as described above is that the identification of and commitment to positive NPV projects theoretically immediately increases the value of the firm to a potential investor. This is because the positive NPV project necessarily increases the present value of the estimated future cash flows of the business itself, which is the thing the investor is assessing to determine what price he will pay in exchange for an invested share in the business.

Why this matters for a football club

I’ll pause for now because essentially the assertion of this whole first set of letters is that largely what a GM or a sporting director of a football club is doing when evaluating player recruitment decisions is he is capital budgeting. While the metric that a businessman uses to assess “go” or “no-go” decisions on various projects is the net present value of the project naturally denominated in the local currency, I recommend that a sporting director adopt a framework whereby the value of a player is estimated using an analogous logic, and that the “go” or “no-go” decisions are expressed in the Absolute Units (smirk) of expected “marginal goal difference,” outputs which are calculated based on insights from the recruitment team’s scouts and data analysts. Essentially, signing a player who will increase your team’s goal difference more than other readily available players increases the competitive value of the team (in goals), and indirectly the overall value of the club itself (in dollars), and vice versa.

Where we go from here will be a step by step explanation of the linkages between some of these fundamental finance and accounting building blocks to the equivalent football information, concepts, and judgments so that we can build a valuation model for a General Manager that is denominated in goal difference.

The next post is going to double click briefly into how a financial analyst develops a projection of estimated future cash flows for a given investment opportunity by breaking it down into five steps.

Congratulations, if you made it all the way to the end, claim this clip as your prize, just like Jaime Carragher claimed this prize at the very end of his career:

Thanks as always for reading. Please share with anyone else you think might be interested in this sort of thing.